Discrete Random Variables

Discrete Random Variable

A discrete random variable is a mapping X of all of the outcomes of a sample space to numerical values x \in \mathbb{Z}.

X: Outcome \in Sample \ Space \to x \in \mathbb{Z}

Probability Mass Function (PMF)

A probability mass function (PMF) is a mapping of values x of discrete random variables X to probabilities [0,1].

p_{X}(x) = P(X = x)

PMF has properties: p_{X}(x) \geq 0, \quad \sum_{x} p_{X}(x) = 1

Cumulative Distribution Function (CDF)

The cumulative distribution function (CDF) for discrete random variables is defined as:

F_{X}(x) = P(X \leq x) = \sum_{k \leq x} p_{X}(k)

Relation to PMF: p_{X}(x) = \frac{dF_{X}(x)}{dx}

F_{X}(x) = \sum_{k \leq x}p_{X}(k)

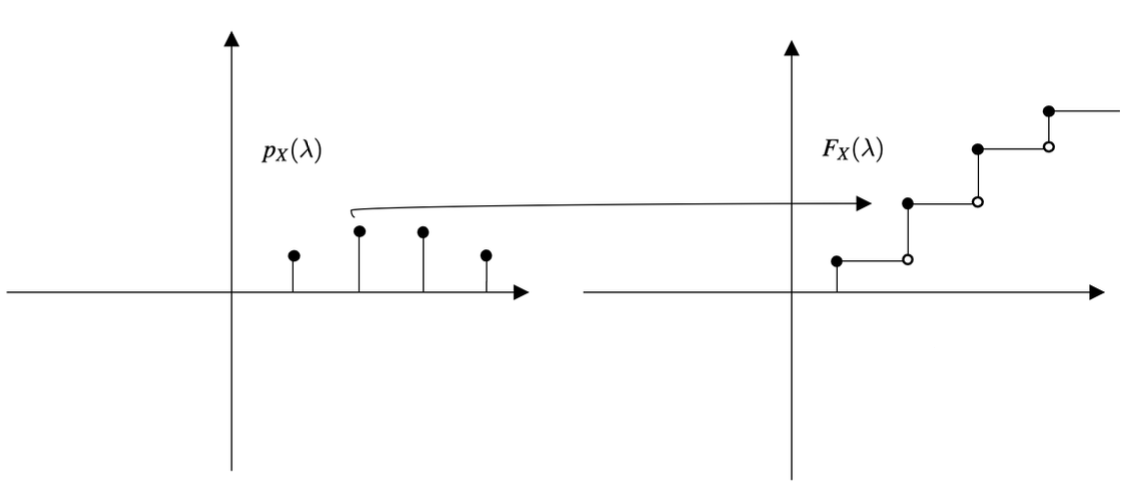

Illustration: PMF and CDF

Expectation and Variance of PMFs

Discrete expectation, or mean, is the average numerical value that the discrete random variable takes over the PMF. E[X] = \sum_{x} x \ p_{X}(x)

Discrete variance is the expected squared difference from the mean of a PMF. Var[X] = E[(X - E[X])^{2}] = \sum_{x}(x - E[X])^2 p_{X}(x)

Joint and Marginal PMFs

The joint PMF calculates the intersection of two discrete random variables: p_{X,Y}(x_{1},x_{2}) = P(X = x_{1}, Y = x_{2})

From the previous definition we can also compute the marginal PMF for a particular random variable: p_{X}(x_{1}) = \sum_{x_{2}} p_{X,Y}(X = x_{1},Y = x_{2})

Conditional Expectation of PMFs

The conditional PMF gives the probability distribution of a discrete random variable given that another variable has a specific value. p_{X|Y}(x_{1}| x_{2}) = \frac{p_{X,Y}(x_{1}, x_{2})}{p_{Y}(x_{2})}

The conditional expectation is the expected value of a discrete random variable given that another variable is fixed at a specific value. E[X| Y = x_{2}] = \sum_{x_{1}} x_{1} \frac{p_{X,Y}(x_{1}, x_{2})}{p_{Y}(x_{2})}

Independence

Two discrete random variables are independent if:

p_{X,Y}(x_{1}, x_{2}) = p_{X}(x_{1}) p_{Y}(x_{2})

For multiple discrete random variables: p_{X_{1},...,X_{n}}(x_{1}, ..., x_{n}) = p_{X_{1}}(x_{1}) ... \ p_{X_{n}}(x_{n})